Warren Buffett, For Sure — You, Maybe Not

Recently, an Investment Management client of Koch Capital asked me to review this NY Times article regarding the author’s recommendation that individuals with a sufficiently long holding period should be 100% invested in stocks. You may be wondering why am I discussing asset allocation in a retirement planning blog?

In this post, I’ll demonstrate why the two disciplines, investment management and retirement planning, should be integrated to achieve financial security for savers aspiring to retire some day. Also in this analysis, we’ll provide guidance on whether you should be 100% invested in stocks in your pre-retirement and post-retirement portfolios.

Are You In or Near Retirement?

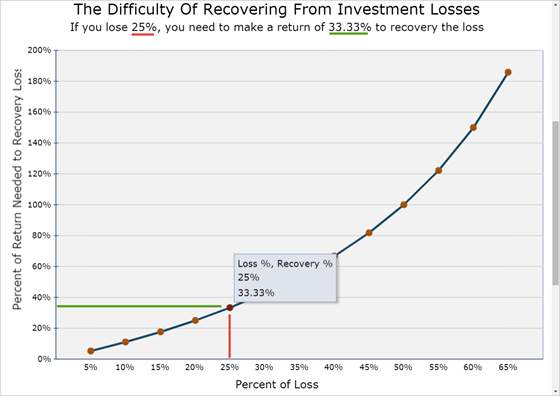

If you are retired or near retirement and are taking regular distributions from your portfolio(s) to fund living expenses, then you are subject to sequence risk. If you draw down a portfolio during a multi-year bear stock market, then your future portfolio distributions plans may be in jeopardy if your portfolio cannot recover during the subsequent good times. The asymmetric nature of compounding works against you when recovering from a portfolio loss; taking distributions in a down market just exacerbates the problem.

Click here to access the full screen view of this image

Source: Koch Capital

Many financial advisors make the distinction between accumulators, or households saving for retirement, and decumulators who are basically retirees taking distributions. If your household is in accumulation mode, then NY Times author makes a good argument to stay 100% in common stocks as long as you can stomach the volatility. The problem with this advice for accumulators is the transition period from accumulation (saving) mode to decumulation (distribution) mode.

As uber financial researcher Michael Kitces points out in this article, sequence of return risk impacts accumulators too, not just decumulating retirees. For example, if you are planning to retire in four years and if you experience a major bear stock market in three years from now, then you may find that your 100% in stocks nest egg will be insufficient to fund your future expected living expenses.

Ignore Current Stock Market Valuations at Your Own Peril

Since it is impossible to perfectly time the stock market (when to buy and when to sell), investors can still strive to better understand the true intrinsic value of the stock market, and the probabilities of future stock market returns based on current valuations.

You have a higher likelihood of future stock portfolio outperformance when valuations are low (and you buy) versus when the stock market is pricey (unless you’re selling). A collective reader duh is warranted here.

In my opinion, it doesn’t matter if you consider yourself a passive investor or not. You WILL become an active investor, whether you mean to or not, during your personal accumulator-to-decumulator transition journey. Failure to plan for this critical transition period may result in pushing back your retirement date in order to cover any savings shortfall. Likewise, your transition period may be a non-event if the market valuation gods are on your side.

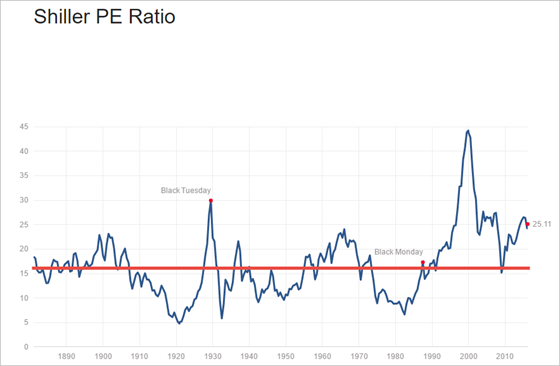

The Shiller Price-to-Earnings (PE10) ratio is one of many valuation measures to help you evaluate whether the stock market is expensive or cheap. While this measure does not possess short-term predictive powers, it is helpful for planning your retirement asset allocation when transitioning from investing for accumulation to investing for decumulation where income consistency and sustainability rule the day. Thus, retirees and near retirees may not want to be 100% in stocks when the Shiller PE ratio is significantly above its long-term average of 16 (red line).

Your Risk Capacity Matters More Than Your Risk Tolerance

So far we haven’t mentioned risk tolerance, the common investor behavioral measure of whether a particular portfolio allocation is “appropriate” for you in terms of volatility. Simply put, your portfolio risk “preference” doesn’t mean squat if your capacity for risk can’t support your tolerance for risk. Warren Buffett can afford to be 100% invested in stocks. If he loses a billion dollars in any given year, his lifestyle remains intact. Mr. Buffett’s high capacity for risk affords him this high level of outcome certainty regardless of his tolerance for investment risk. It’s good to be Warren.

At Koch Capital, we use the straightforward concept of retirement fundedness (a.k.a. the funded ratio) to measure your risk capacity in terms of a simple ratio. The funded ratio measures your total current savings against your future expected retirement living expenses. The higher your funded ratio, the more risk capacity you have. A funded ratio greater than 1 means you have sufficient assets to cover your liabilities. I’m guessing that Mr. Buffett has a 1000 or higher funded ratio which is why the question of his risk tolerance associated with his 100% stock allocation is moot.

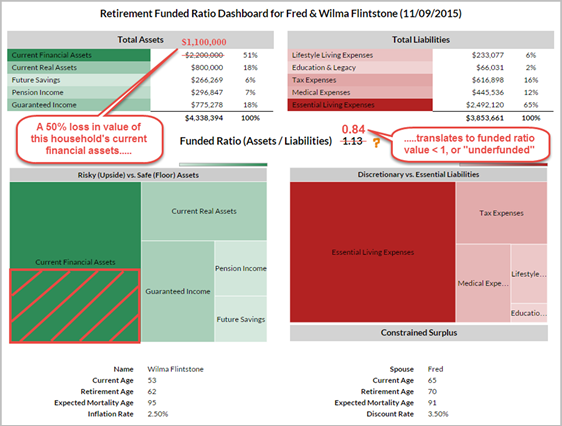

Let’s look at an example of risk capacity in action. The year is 2007. Wilma and Fred Flintstone wish to retire in 2008. They are currently 100% invested in stocks across all their investment accounts (IRAs, 401ks, brokerage, etc.) for a total current financial asset value of $2.2 million (see balance sheet summary below). This asset balance represents over 50% of Wilma and Fred’s total asset base.

Source: Koch Capital

The Great Recession hits. Wilma and Fred’s $2.2M aggregate balance is cut in half to $1.1M. Their original plan to start regular distributions in 2008 to fund their living expenses is now in question, and potentially unsustainable over their expected lifespans.

While the exact unfortunate timing of Wilma and Fred’s desired retirement date occurs infrequently in real life, the consequence is severe. The good news is that this scenario is fixable. Households can reduce their chance of an extreme portfolio loss event (see max drawdown definition) affecting their retirement plans by reducing their 100% stock exposure prior to retirement. Alternatively, households can also choose convert part of their current financial assets to safe(r) pension assets like guaranteed annuity contracts and individual Treasury bond ladders, as well as maintain a cash reserve to cover living expenses in a downturn allowing their portfolios to recover.

While Wilma and Fred may have exhibited an aggressive risk preference for a 100% stock allocation, their recalculated funded ratio value of 0.84 (reduced risk capacity) may prove insufficient to keep them on their original retirement track. They may have to consider delaying retirement to save more and allow their portfolios to recover. Ideally, we prefer to see their funded value rise to 1.2 or higher, our overfunded status before commencing with retirement (see Terminology page for further explanations).

Decision Considerations for the 100%-in-Stocks Investor

In my opinion, evaluate your expected retirement date, risk capacity via your funded ratio, and current market valuations before considering your risk preference when determining your portfolio’s stock allocation.

If you are years away from retirement, go ahead with a 100% stock allocation, preferably implementing a broad global asset class approach using low-cost index funds as your core holdings. Remember that your ability to earn income during your pre-retirement years raises your capacity for risk.

If you are nearing retirement and current market valuations are rich, consider dialing back your stock allocation to maintain a sufficient reserve to fund living expenses for one to two years in case of a severe market downturn, or to potentially re-invest in stocks when valuations are more favorable.

If you are very near retirement, current market valuations are favorable, and your funded ratio is already over 1.20, then you’re in the catbird seat. In this case, you can base your stock allocation decision on your risk preference, and get a good night’s sleep whether you are 100% in stocks or more conservatively invested.

Obviously, there are thousands of subtle permutations regarding your proximity to retirement, the fluidity of your risk capacity over time and the degree of current market over or under valuation, which is why I love being a financial advisor. Every household is different, every retirement plan is unique, and every engagement is opportunity to help families in a meaningful way.

Thank you for your continued support and interest......Jim

Additional Resource Links

New York Times 02-12-2016 stock allocation article:

Michael Kitces Shiller CAPE Market Valuation article:

Russell Research: Adaptive Investing paper:

Zvi Bodie 10-90 Retirement Investing: A New Approach paper:

Michael Kitces Sequence of Returns Risk for Accumulators article:

My Retirement Income video which demonstrates sequence risk:

About Jim Koch

Jim Koch is the Founder and Principal of Koch Capital Management, an independent Registered Investment Advisor (RIA) in the San Francisco Bay Area. He specializes in providing customized financial solutions to individuals, families, trusts, business entities and other advisers so they are better able to achieve their goals. Jim sees himself as an “implementer” of financial innovation, using state-of-the-art technology to provide practical investment management and retirement planning solutions for clients.

General Disclosures

This information is provided for informational/educational purposes only. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions. Nothing presented herein is or is intended to constitute advice to use or buy any of third-party applications presented here, and no purchase decision should be made based on any information provided herein. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Third Party Information

While Koch Capital has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, timeliness, or completeness of third party information presented herein. Any third party trademarks appearing herein are the property of their respective owners. At certain places on this website, live 'links' to other Internet addresses can be accessed. Koch Capital does not endorse, approve, certify, or control the content of such websites, and does not guarantee or assume responsibility for the accuracy or completeness of information located on such websites. Any links to other sites are not intended as referrals or endorsements, but are merely provided for convenience and informational purposes. Use of any information obtained from such addresses is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy, and timeliness.

No comments:

Post a Comment