A Sequential Random Journey

In this recent blog post, Dirk Cotton of the Retirement Cafe blog explains why retirement planning is never a set and forget type of endeavor. He uses the metaphor of a sailboat on a long journey. At the end of each day, the sailor needs to correct her course to account for drift. Of course, this also assumes that the sailor has a planned destination in the first place?

At Koch Capital, we agree with Mr. Cotton’s analysis and appreciate his symbolism of a sailboat navigating a big ocean. For retirement seeking investors, the destination is to safely fund retirement throughout their lifetimes while maintaining enough flexibility to adapt to life’s unplanned course changes.

Click here to view the full image

Source: Koch Capital

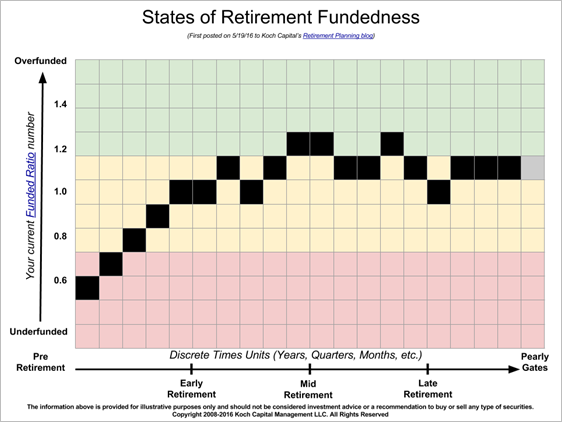

By viewing your retirement journey through the lens of a series of sequential, discrete moves, you can better monitor, in my opinion, your progress and adapt to the “unexpected” throughout your retirement lifecycle.

For example, the state diagram above tracks a household’s level of retirement fundedness (funded ratio) at discrete points in time, usually age related. Having this simple funded status dashboard available to monitor, gives the household a clear picture of where it’s heading and how much drift to correct for.

Monitor and Adjust Course, Then Repeat

What is being described here is a discrete-time Markov chain, where all that matters is where you are now and what life throws at you next. Typically, these processes are memoryless, meaning how you got to your current state is meaningless, and all that counts is where you are heading next. However, when budgeting for future retirement expenses, the past is good place start even if you need to adapt the plan going forward.

The funded ratio, while not a perfect measure of your ability to support your retirement lifestyle at any given moment in time, is a simple and intuitive metric to gauge if your current household asset mix can support your anticipated future retirement expenses. I’m using funded ratio in this hypothetical example as a real-time retirement compass to help you gauge the degree of course drift and in which direction. Please see this post for more details on managing your personal assets and liabilities if interested.

Source: Koch Capital

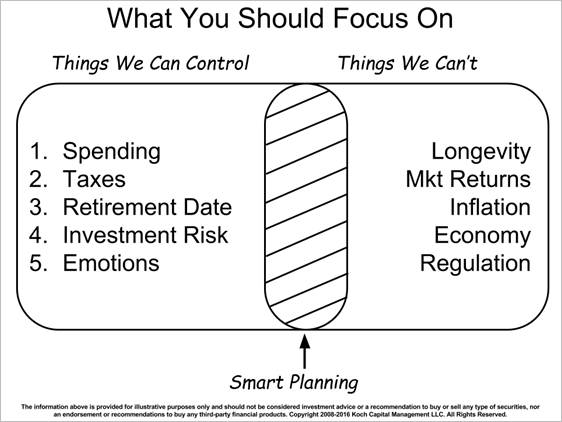

Mr. Cotton also points out the absurdity of forecasting future risky asset returns beyond the near term as well as the necessity of a frequent retirement plan monitoring and updating. Please consider that as much as you may believe you can control your lifespan, stock market returns, consumer inflation, the economy, what Congress will regulate next as well as all the other unexpected life events that get randomly thrown at your household, you have very little actual control beyond your spending, taxes, when you retiree, level of investment risk and your emotional state. This is why planning for what you can control and budgeting a little extra for those things out of your control are key to your retirement funding success.

What Makes a Retirement Plan Good?

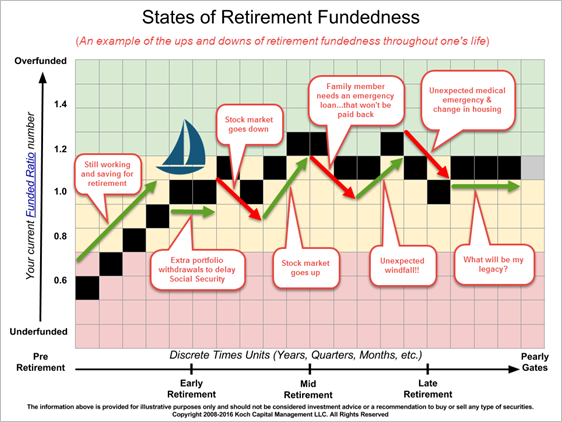

In my opinion, the typical retirement journey is series of forward-looking, sequential moves often responding to life’s unexpected “drifts”, some good and some not. But the destination is the same for all of us, so get a retirement plan that provides the appropriate funding security so you can enjoy the journey. A plan that identifies the drifts early, adapts to life’s course corrections quickly, and keeps your rational brain informed, is a plan that will support you in making the right financial decisions for your household.

Source: Koch Capital

About Jim Koch

Jim Koch is the Founder and Principal of Koch Capital Management, an independent Registered Investment Advisor (RIA) in the San Francisco Bay Area. He specializes in providing customized financial solutions to individuals, families, trusts, business entities and other advisers so they are better able to achieve their goals. Jim sees himself as an “implementer” of financial innovation, using state-of-the-art technology to provide practical investment management and retirement planning solutions for his clients.

General Disclosures

This information is provided for informational/educational purposes only. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions. Nothing presented herein is or is intended to constitute advice to use or buy any of third-party applications presented here, and no purchase decision should be made based on any information provided herein. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Third Party Information

While Koch Capital has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, timeliness, or completeness of third party information presented herein. Any third party trademarks appearing herein are the property of their respective owners. At certain places on this website, live 'links' to other Internet addresses can be accessed. Koch Capital does not endorse, approve, certify, or control the content of such websites, and does not guarantee or assume responsibility for the accuracy or completeness of information located on such websites. Any links to other sites are not intended as referrals or endorsements, but are merely provided for convenience and informational purposes. Use of any information obtained from such addresses is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy, and timeliness.

No comments:

Post a Comment