It’s a Bird…It’s a Plane...It’s HSA-man!

Recently, several respected personal financial sources have written about the benefits and costs associated with implementing a Health Savings Account (HSA) plan. Since the HSA plan details are available in the sourced articles at end of this post, I will focus on several important HSA implementation considerations.

Recently, several respected personal financial sources have written about the benefits and costs associated with implementing a Health Savings Account (HSA) plan. Since the HSA plan details are available in the sourced articles at end of this post, I will focus on several important HSA implementation considerations.

I love the HSA concept and have personally implemented an HSA plan for my family. However, these plans only make sense, in my humble opinion, if (1) you are 55 or younger, (2) you and your family are in great health, (3) you have or can find a High-Deductible Health Plan (HDHP) and insurance provider that you actually like, (4) you have already maxed out your 401k/IRA contributions, and (5) you have enough after-tax annual cash flow to pay up to your deductible as well as any typical out-of-pocket medical expenses in a given year.

The Ultimate Delay of Gratification

The key is not to use your annual HSA contributions right away and instead stay invested for as long as possible to benefit from tax-free compounding. This is a very high bar!!! But if you can swing it, then it’s a great way to save for future medical expenses, especially late in retirement when medical expenses are generally at their highest.

Source: Koch Capital

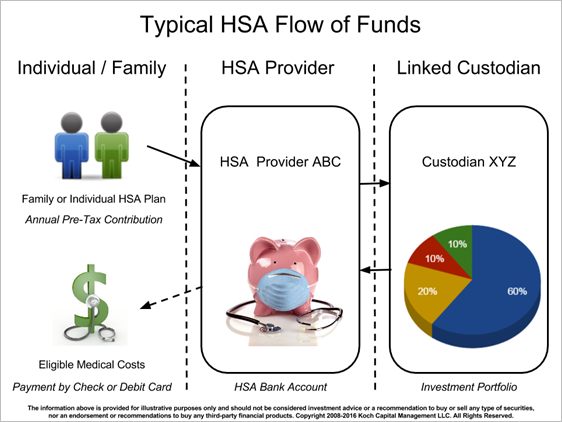

Typical HSA Plan Flow of Funds

In your typical HSA plan, you make annual contributions to your HSA provider. For 2016, the family plan tax-deductible contribution limit is $6,750, or $7,750 if you are 55 or older. The diagram below provides the typical flow of funds within the HSA plan structure. Please note that HSA Provider and Linked Custodian may belong to the same organization; I’ve separated them to highlight the administrative/banking side versus the investment side.

Source: Koch Capital

If you are fortunate enough to deposit the maximum contribution limit annually to your HSA bank account and immediately invest it, then you essentially have the functional equivalent of a contributory IRA for building up tax-free savings, and a Roth IRA on the withdrawal side if making eligible medical payments.

In my case, I started my HSA in 2007 and invested all annual contributions, except for one year when my wife and I decided use that year’s contribution amount along with the residual HSA bank balance to pay for an unexpected medical expense. Please note that most HSA providers require that you keep a minimum cash balance on the bank account side to avoid monthly account fees.

Several Parting Thoughts

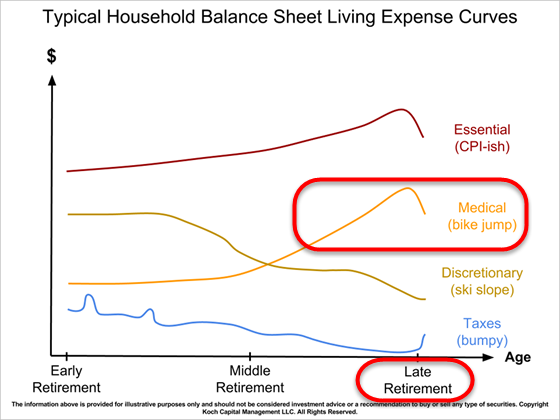

Within our retirement planning framework, Koch Capital strives to have at least one long-term funding source to help with late-in-life expenses that come from living longer than you expect (longevity risk). Whether it’s an HSA, Roth IRA, long-term care insurance (LTCI) and/or life insurance, the optimal mix varies from household to household depending on your household’s unique retirement goals, current health and available financial resources.

|  |

Under our Household Balance Sheet (HHBS) accounting methodolgy, your current HSA balance is maintained as a current financial asset and is matched against future budgeted medical expenses on the liability side.

Life happens….especially in the arena of late-in-life unexpected medical expenses. Having a tax-efficient, supplemental medical funding source, whether an HSA, a Roth or insurance, is a valuable asset if you plan earlier and stay the course.

Thank you for your continued interest......Jim

Additional HSA Resources

Wall Street Journal 01-30-2016 HSA article:

Michael Kitces 01-20-2016 HSA article:

HSA Bank Standard Fees and Interest Schedule:

IRS Publication 969 Health Savings Accounts:

About Jim Koch

Jim Koch is the Founder and Principal of Koch Capital Management, an independent Registered Investment Advisor (RIA) in the San Francisco Bay Area. He specializes in providing customized financial solutions to individuals, families, trusts, business entities and other advisers so they are better able to achieve their goals. Jim sees himself as an “implementer” of financial innovation, using state-of-the-art technology to provide practical investment management and retirement planning solutions for clients.

General Disclosures

This information is provided for informational/educational purposes only. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions. Nothing presented herein is or is intended to constitute advice to use or buy any of third-party applications presented here, and no purchase decision should be made based on any information provided herein. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Third Party Information

While Koch Capital has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, timeliness, or completeness of third party information presented herein. Any third party trademarks appearing herein are the property of their respective owners. At certain places on this website, live 'links' to other Internet addresses can be accessed. Koch Capital does not endorse, approve, certify, or control the content of such websites, and does not guarantee or assume responsibility for the accuracy or completeness of information located on such websites. Any links to other sites are not intended as referrals or endorsements, but are merely provided for convenience and informational purposes. Use of any information obtained from such addresses is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy, and timeliness.

No comments:

Post a Comment