Present Value vs. Future Value

The purpose of this blog post is to help explain the use of the discount rate in the funded ratio calculation. Since Kiplinger first published its Retirement Security in a Single Number article on April 1st, I have received over 400 requests (thank you) for Koch Capital’s Funded Ratio Demo template. And by far the most frequent question as well as the most confusing aspect of the Household Balance Sheet (HHBS) approach to retirement planning involves the selection of an appropriate discount rate and understanding its relationship with your other growth assets’ future returns.

First, a quick review of present value versus future value and the time value of money. If you had your choice between receiving $1 today or receiving $1 in five years, which option would you choose? The rational person would choose $1 today given that $1 in the future would be worth less given the possibility of inflation reducing its purchasing power and the uncertainty in the collection of a future asset five years from now.

First, a quick review of present value versus future value and the time value of money. If you had your choice between receiving $1 today or receiving $1 in five years, which option would you choose? The rational person would choose $1 today given that $1 in the future would be worth less given the possibility of inflation reducing its purchasing power and the uncertainty in the collection of a future asset five years from now.

For the rational person to take the future $1 option, she would require a “discounted” value, like 85¢ on the dollar, to compensate her for the additional risk of owning a future asset. She might derive that number by calculating a “hurdle rate” depending on what she could earn on that $1 today over the next five years, then discounting the future $1 by that hurdle rate to determine the reduced amount she would be willing to pay today for the future $1 given the uncertainties of inflation and mortality.

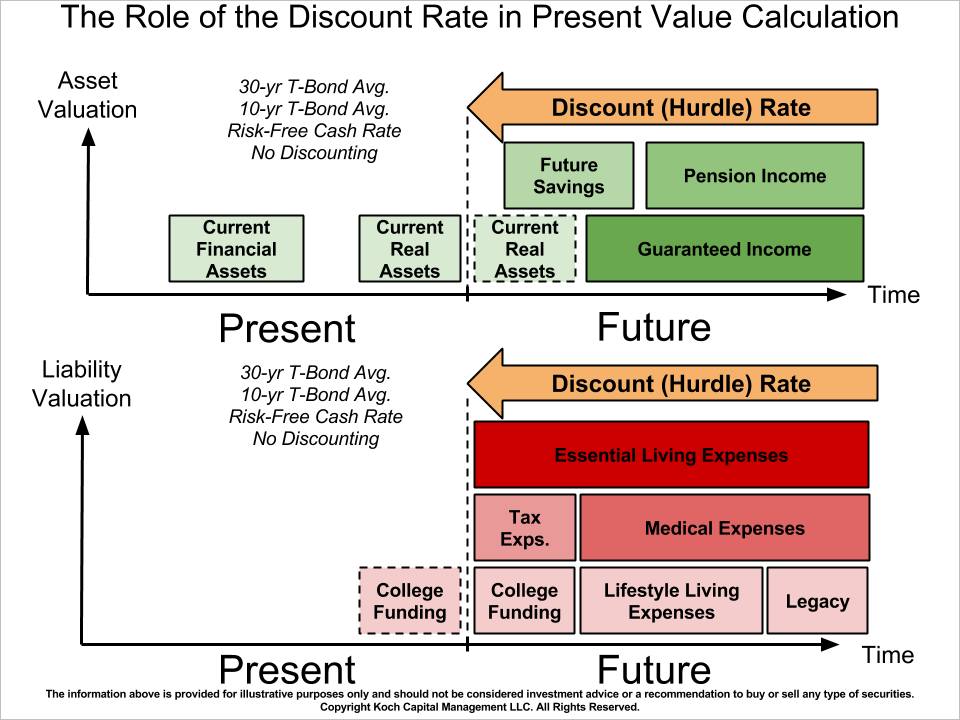

In the case of the HHBS approach (see diagram below), Koch Capital is using the present value or fair market value (FMV) of your Current Financial Assets and Current Real Assets against your future liabilities. We need to get those future liabilities as well as any future income streams discounted back into present value equivalents so we can run the funded ratio calculation.

Source: Koch Capital

Risky Asset Dependency & Time

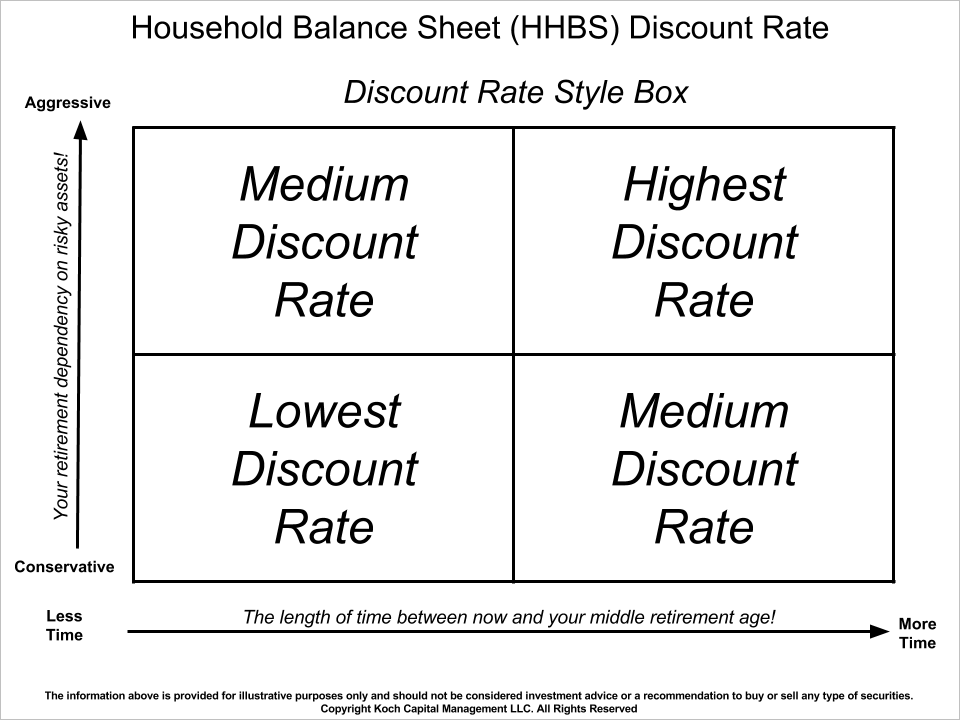

When considering what discount (hurdle) rate to select for your Funded Ratio Demo exercise, it’s useful to think along the two dimensions of time and dependency on risky assets. I’m defining risky assets here as your investment portfolio(s), your home, a private business, etc. Essentially, it’s your asset base that tends to fluctuate in price from year to year and has no trusted counterparty guarantee of a regular payout.

Therefore, the more dependency you have on risky assets to fund your retirement, the higher the discount rate you should choose, all else being equal. However, there’s a catch. Increasing your discount rate also increases the chance of plan failure if you can’t achieve your hurdle rate for the duration of the target liability.

Remember that your Funded Ratio Demo discount rate is a composite rate reflecting not just the hurdle rate of your portfolio returns, but also your home appreciation rate (the long term average is 3%) and possibly private business growth too.

Source: Koch Capital

Likewise, the time factor of the discount rate is important too. In general, the further you are away your planned retirement date, the higher discount rate you should use to account for the possibility of future inflation and the uncertainty of future income collection (or required payment in the case of a future liability).

With the time factor in mind, here’s a rule-of-thumb (ROT) to help Funded Ratio Demo participants calculate their composite discount rate. I have no empirical data to back up this methodology. Nevertheless, I still believe that Funded Ratio Demo participants will find this ROT helpful given the understandable confusion surrounding discount rate usage in the HHBS model.

First, determine your middle retirement age, or the midpoint age between your retirement age and your expected mortality age. Your middle retirement age choice should reflect your high conviction of living to at least that age, barring any unexpected life threatening emergency. Your middle retirement age will probably fall somewhere between the ages of 72 and 84.

Select Treasury rates as 4/13/2015; Your rates will be different!

Source: Koch Capital, Google Finance

Next, calculate the spread in years between your current age and your middle retirement age. If that number is less than 5 years, start with the 1-4 Year Treasury rate in Step #6 of the Funded Ratio Demo as your baseline discount rate. If the spread is between 5 and 10 years, start with the 5 Year Treasury rate. If the spread is between 10 and 20 years, then use the 10 Year Treasury rate provided in Step #6. Finally, if the spread is over 20 years, use the 30 Year Treasury rate as your discount rate starting point. Now, let’s see if an additional discount rate adjustment is warranted based on your dependency on risky assets.

How Lucky Do You Feel?

Please remember that this first iteration the Funded Ratio Demo is definitely more educational than functional given the inherent complexities of do-it-yourself retirement planning. Each Funded Ratio Demo participant will have a unique allocation mix of risky growth assets and safe(r) income assets. If the concept of risky versus safe assets is unfamiliar to you, please review the Retirement Funded Ratio video before proceeding.

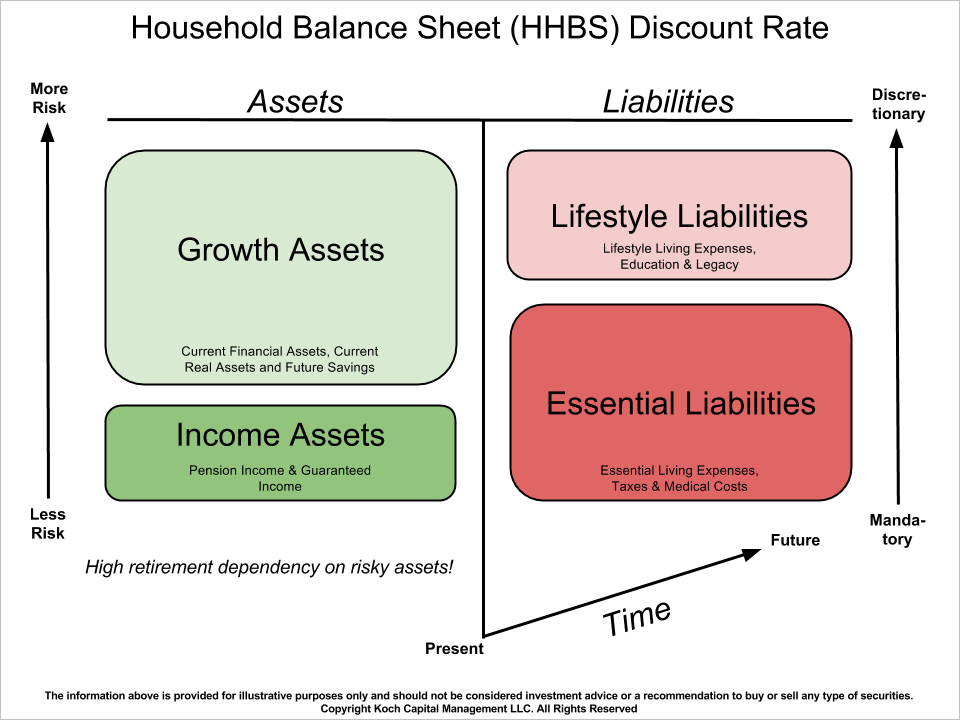

Your personal retirement dependency on risky assets is shown in the Funded Ratio Demo dashboard section with the two colored pie charts. If your left side asset pie chart is displaying a higher proportion of light green risky assets than dark green safe assets, then you have a higher dependency on risky assets than safe assets. The stylized balance sheet diagram below provides a simple visual to help explain the dependency concept.

Source: Koch Capital

This allocation mix above is typical. Most young savers as well as older savers comfortable taking on additional stock market risk for the chance of additional future retirement dollars, will tilt their retirement allocations toward riskier pools of growth assets—Current FInancial Assets, Current Real Assets and Future Savings in the HHBS model.

If you fall into this category of Funded Ratio Demo participant, you may or may not want to consider a small upward adjustment to your discount rate calculated earlier based on just your time component. This adjustment is very nuanced and totally optional. I can’t provide an exact formula to calculate it given this reaches into the proprietary methods Koch Capital uses to determine discount values for its clients. However, if you can accept the additional risk that you are potentially funding part or all of your essential future living expenses with risky assets, then please feel free to nudge up (increase) your time-based discount rate.

More Conservative Approach

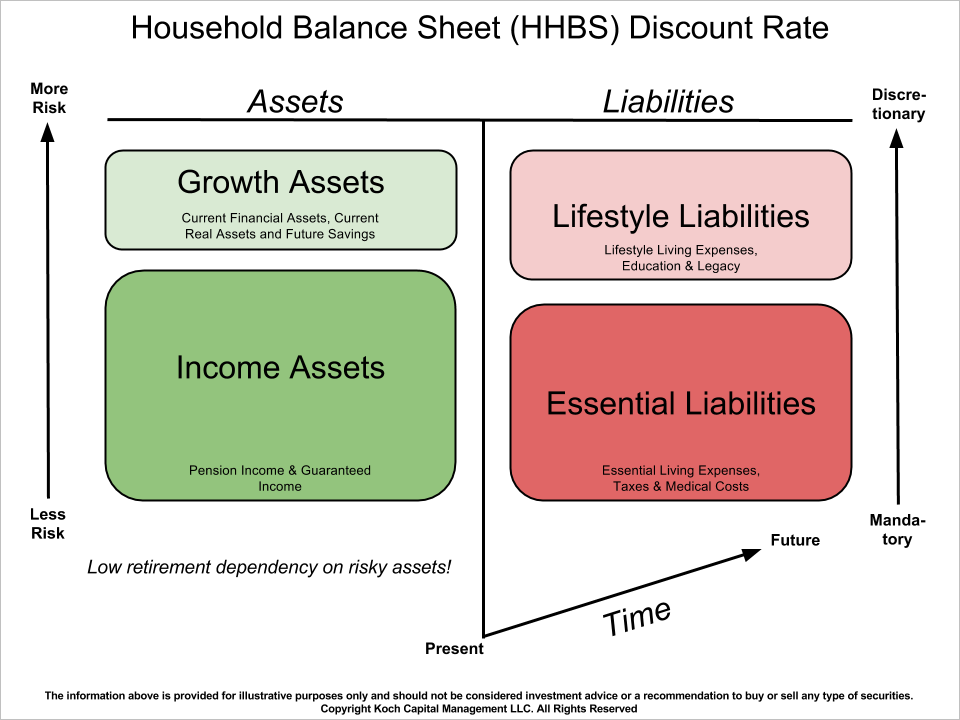

For our regular retirement planning clientele, Koch Capital prefers at a minimum to have sufficient, safer income assets to cover the budgeted future essential retirement expenses at the start of retirement. This is not always possible, but highly desirable if you wish to reduce your chance of running out of money in retirement.

Source: Koch Capital

In summary, a Funded Ratio Demo participant already holding more conservative (safer) income assets can choose a more conservative (lower) composite discount rate, all else being equal. The time-based discount rate suggestion, without any risky asset dependency adjustment, is probably sufficient.

Please don’t make yourself too crazy with your personal discount rate calculation. Yes, it’s important. But your expected mortality age estimate will have a bigger impact on your funded ratio calculation, so please make sure to give it careful consideration too.

Finally, please remember that the Funded Ratio Demo exercise is a single snapshot in time. In the full HHBS implementation, the model is updated daily with current portfolio balances, interest rate changes and inflation data to provide on-going and proactive retirement management.

Thank you for your continued Funded Ration Demo interest and happy discounting....Jim

About Jim Koch

Jim Koch is the Founder and Principal of Koch Capital Management, an independent Registered Investment Advisor (RIA) in the San Francisco Bay Area. He specializes in providing customized financial solutions to individuals, families, trusts, business entities and other advisers so they are better able to achieve their goals. Jim sees himself as an “implementer” of financial innovation, using state-of-the-art technology to provide practical investment management and retirement planning solutions for clients.

General Disclosures

This information is provided for informational/educational purposes only. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions. Nothing presented herein is or is intended to constitute advice to use or buy any of third-party applications presented here, and no purchase decision should be made based on any information provided herein. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Third Party Information

While Koch Capital has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, timeliness, or completeness of third party information presented herein. Any third party trademarks appearing herein are the property of their respective owners. At certain places on this website, live 'links' to other Internet addresses can be accessed. Koch Capital does not endorse, approve, certify, or control the content of such websites, and does not guarantee or assume responsibility for the accuracy or completeness of information located on such websites. Any links to other sites are not intended as referrals or endorsements, but are merely provided for convenience and informational purposes. Use of any information obtained from such addresses is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy, and timeliness.

No comments:

Post a Comment